Estimate USDJPY after 1 day based on 10 years of data by using scikit-learn

# import libraries import pandas as pd import numpy as np import talib as ta from sklearn.model_selection import train_test_split from sklearn.ensemble import RandomForestClassifier from sklearn.metrics import accuracy_score, precision_score, recall_score, confusion_matrix import optuna import matplotlib.pyplot as plt import seaborn as sns

# Check the shape print(df0.shape)

# Check the data summary = df0.describe() print(summary)

# # Display information about the DataFrame df0.info()

df0["Date"] = pd.to_datetime(df0["Date"])

# Get the oldest and latest dates

oldest_date = df0["Date"].min()

latest_date = df0["Date"].max()

print("Oldest Date:", oldest_date)

print("Latest Date:", latest_date)df0["Date"] = pd.to_datetime(df0["Date"])

# Get the oldest and latest dates

oldest_date = df0["Date"].min()

latest_date = df0["Date"].max()

print("Oldest Date:", oldest_date)

print("Latest Date:", latest_date)Oldest Date: 2003-09-15 00:00:00

Latest Date: 2022-11-11 00:00:00

# Load and clean the data for df1

df1 = pd.read_csv("")

df1["Date"] = pd.to_datetime(df1["Date"], format="%m/%d/%Y") # Specify the correct date format

# Concatenate DataFrames

df = pd.concat([df0, df1])

# Calculate oldest and latest dates

oldest_date = df["Date"].min()

latest_date = df["Date"].max()

print("Oldest Date:", oldest_date)

print("Latest Date:", latest_date)Oldest Date: 2003-09-15 00:00:00

Latest Date: 2022-11-11 00:00:00

print(df.shape)

(5218, 7)

df.info()

<class ‘pandas.core.frame.DataFrame’>

Index: 5218 entries, 0 to 217

Data columns (total 7 columns):

# Column Non-Null Count Dtype — —— ————– —–

0 Date 5218 non-null datetime64[ns]

1 Price 5218 non-null float64

2 Open 5218 non-null float64

3 High 5218 non-null float64

4 Low 5218 non-null float64

5 Vol. 0 non-null float64

6 Change % 5218 non-null object

dtypes: datetime64[ns](1), float64(5), object(1) memory usage: 326.1+ KB

# Drop the "Vol." column from df

df = df.drop("Vol.", axis=1)

# Check the shape of df after dropping the column

print("Shape of df after dropping 'Vol.' column:", df.shape)Shape of df after dropping ‘Vol.’ column: (5218, 6)

# Identify columns with all null values

null_columns = df.columns[df.isnull().all()]

# Drop columns with all null values

df = df.drop(columns=null_columns)

# Check the shape of df after dropping null columns

print("Shape of df after dropping null columns:", df.shape)Shape of df after dropping null columns: (5218, 6)

# print the unique column names in df

print("Unique column names in df:", df.columns.tolist())Unique column names in df: [‘Date’, ‘Price’, ‘Open’, ‘High’, ‘Low’, ‘Change %’]

#All subsequent calculations use the closing rate close = np.array(df["Price"]) #Create an empty dataframe to contain features df_feature = pd.DataFrame(index=range(len(df)),columns=["SMA5/current", "SMA20/current","RSI","MACD","BBANDS+2σ","BBANDS-2σ"]) #Ccalculate technical indicators (features used in this training) using talib and put in df_feature #Simple moving average uses the ratio of the simple moving average to the closing price of the day as the feature value df_feature["SMA5/current"]= ta.SMA(close, timeperiod=5) / close df_feature["SMA20/current"]= ta.SMA(close, timeperiod=20) / close #RSI df_feature["RSI"] = ta.RSI(close, timeperiod=14) #MACD df_feature["MACD"], _ , _= ta.MACD(close, fastperiod=12, slowperiod=26, signalperiod=9) #Bollinger bands upper, middle, lower = ta.BBANDS(close, timeperiod=20, nbdevup=3, nbdevdn=3) df_feature["BBANDS+2σ"] = upper / close df_feature["BBANDS-2σ"] = lower / close

df["the day before_float"] = df["Change %"].apply(lambda x: float(x.replace("%", "")))

#How to categorize the % of previous day. Divide as much as possible so that the sample of each class is equal

def classify(x):

if x <= -0.2:

return 'down'

elif -0.2 < x < 0.2:

return 'even'

elif 0.2 <= x:

return 'up'

df["the day before_classified"] = df["the day before_float"].apply(lambda x: classify(x))

#Shift the data you want to teach by one day (you know what I mean)

df_y = df["the day before_classified"].shift()# Reset the index of df0_y to ensure uniqueness df_y = df_y.reset_index(drop=True) # Concatenate df0_feature and df0_y with reset index df_xy = pd.concat([df_feature, df_y], axis=1) df_xy = df_xy.dropna(how="any")

# print("Shape of df_xy:", df_xy.shape)

print("Number of samples in df_xy:", len(df_xy))

X_train, X_test, Y_train, Y_test = train_test_split(

df_xy[["SMA5/current", "SMA20/current", "RSI", "MACD", "BBANDS+2σ", "BBANDS-2σ"]],

df_xy["the day before_classified"],

train_size=0.8,

random_state=42

)

print("Shape of X_train:", X_train.shape)

print("Shape of X_test:", X_test.shape)

print("Shape of Y_train:", Y_train.shape)

print("Shape of Y_test:", Y_test.shape)Shape of df_xy: (5185, 7)

Number of samples in df_xy: 5185 Shape of X_train: (4148, 6)

Shape of X_test: (1037, 6)

Shape of Y_train: (4148,)

Shape of Y_test: (1037,)

X_train, X_test, Y_train, Y_test = train_test_split(df_xy[["SMA5/current", "SMA20/current","RSI","MACD","BBANDS+2σ","BBANDS-2σ"]],df_xy["前日比_classified"], train_size=0.8)

def objective(trial):

min_samples_split = trial.suggest_int("min_samples_split", 2,16)

max_leaf_nodes = int(trial.suggest_discrete_uniform("max_leaf_nodes", 4,64,4))

criterion = trial.suggest_categorical("criterion", ["gini", "entropy"])

n_estimators = int(trial.suggest_discrete_uniform("n_estimators", 50,500,50))

max_depth = trial.suggest_int("max_depth", 3,10)

clf = RandomForestClassifier(random_state=1, n_estimators = n_estimators, max_leaf_nodes = max_leaf_nodes, max_depth=max_depth, max_features=None,criterion=criterion,min_samples_split=min_samples_split)

clf.fit(X_train, Y_train)

return 1 - accuracy_score(Y_test, clf.predict(X_test))

study = optuna.create_study()

study.optimize(objective, n_trials=100)

print(1-study.best_value)

print(study.best_params)# Create and train a RandomForestClassifier

model = RandomForestClassifier()

model.fit(X_train, Y_train)

# Predict the target values for the test data

Y_pred = model.predict(X_test)

# Calculate the accuracy, precision, recall

accuracy = accuracy_score(Y_test, Y_pred)

precision = precision_score(Y_test, Y_pred, average='weighted') # You can also use 'macro' or 'micro'

recall = recall_score(Y_test, Y_pred, average='weighted') # You can also use 'macro' or 'micro'

print("Accuracy:", accuracy)

print("Precision:", precision)

print("Recall:", recall)Accuracy: 0.5660559305689489

Precision: 0.5637978876125685

Recall: 0.5660559305689489

# Create and train a RandomForestClassifier

model = RandomForestClassifier(n_estimators=100, random_state=1)

model.fit(X_train, Y_train)

# Get feature importances

feature_importances = model.feature_importances_

# Create a DataFrame to associate features with their importances

importance_df = pd.DataFrame({"Feature": X_train.columns, "Importance": feature_importances})

importance_df = importance_df.sort_values(by="Importance", ascending=False)

# Print or visualize the feature importances

print(importance_df)

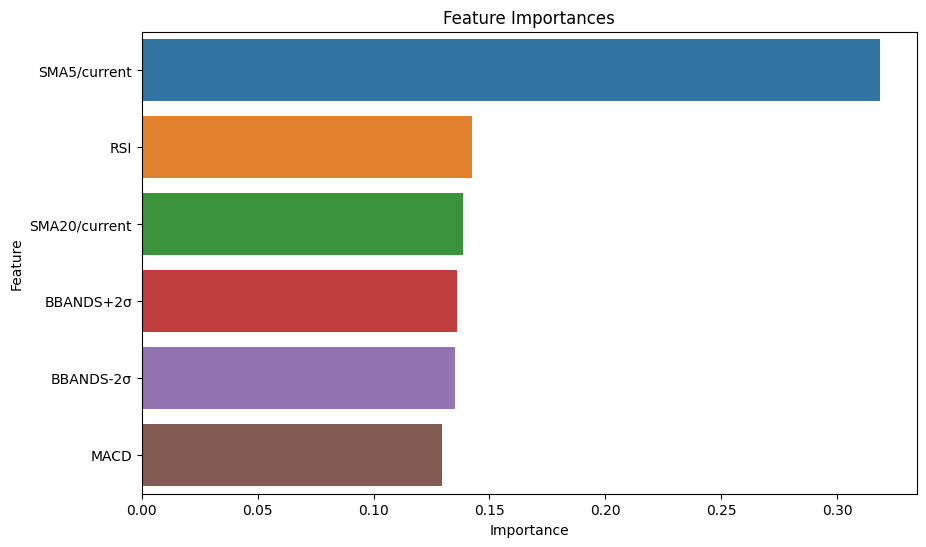

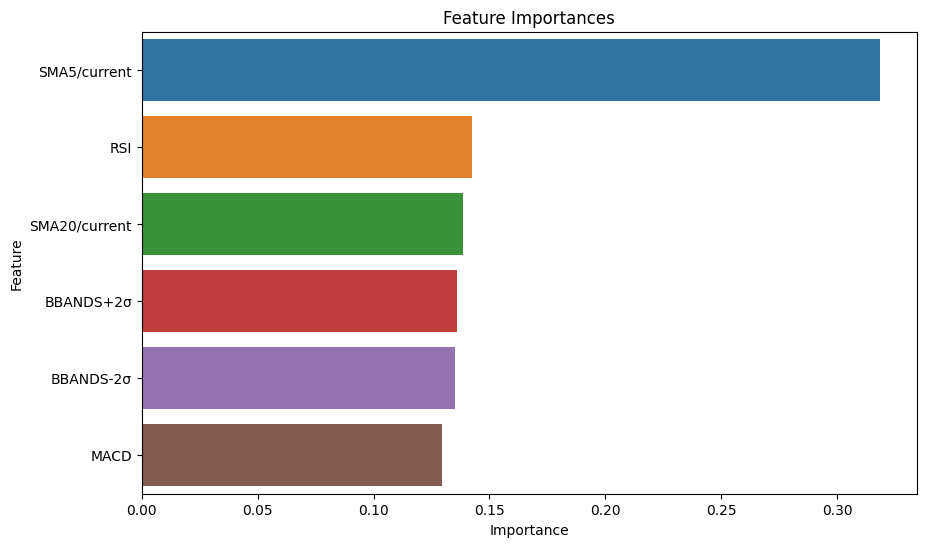

plt.figure(figsize=(10, 6))

sns.barplot(x="Importance", y="Feature", data=importance_df)

plt.title("Feature Importances")

plt.xlabel("Importance")

plt.ylabel("Feature")

plt.show() Feature Importance

0 SMA5/current 0.318452

2 RSI 0.142284

1 SMA20/current 0.138512

4 BBANDS+2σ 0.135807

5 BBANDS-2σ 0.135339

3 MACD 0.129607