Forex Forecasting with Random Forests 2/N – Technical indicators

Economy

## Feature creation/processing

#- Addition of technical indicators

#- Creation of statistics that may be valid for each variable

#- Differences in historical performance (e.g. price difference from a week ago)

#- Date processing (e.g. holidays, days of the week)

## Feature creation/processing

#- Addition of technical indicators

#- Creation of statistics that may be valid for each variable

#- Differences in historical performance (e.g. price difference from a week ago)

#- Date processing (e.g. holidays, days of the week)

# Technical indicators to be calculated

Date = np.array(df_drop['Date'])

high = np.array(df_drop['eurusd_High'])

low = np.array(df_drop['eurusd_Low'])

close = np.array(df_drop['eurusd_Close'])

prefix = 'eurusd'

# Additional technical indicators

df_technical_indicators = calc_technical_indicators(Date, high, low, close, prefix)

df_drop_add = pd.merge(df_drop

,df_technical_indicators

,on='Date'

,how='left').dropna(how="any")

print(df_drop_add.shape)

### Date processing

# Extract date year, month and day of the week (0 for Monday, 6 for Sunday) information

# Convert to dummy variable

df_drop_add =df_drop_add.assign(

# year=df_drop['Date'].dt.year

month=df_drop['Date'].dt.month

,weekday=df_drop['Date'].dt.dayofweek

).pipe(lambda df: pd.get_dummies(df, columns=['month','weekday']))

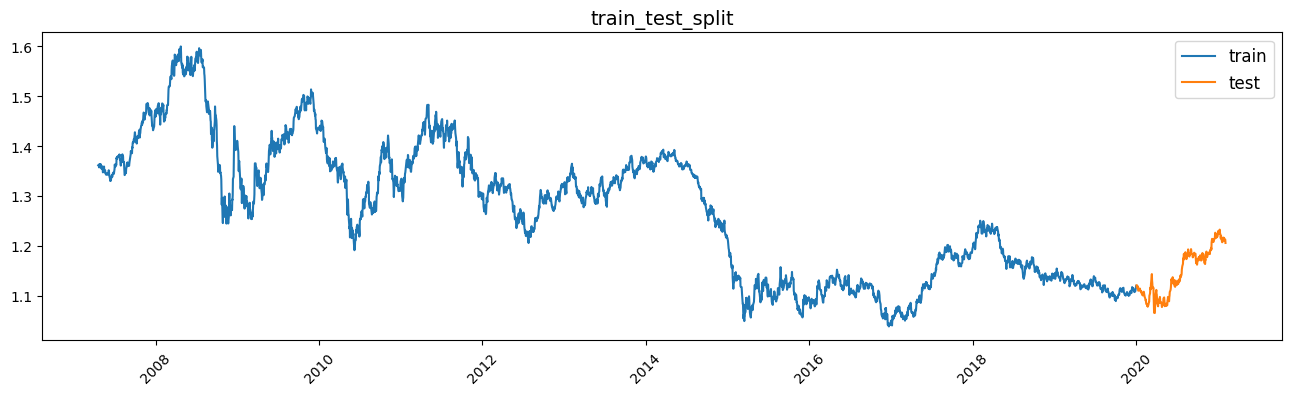

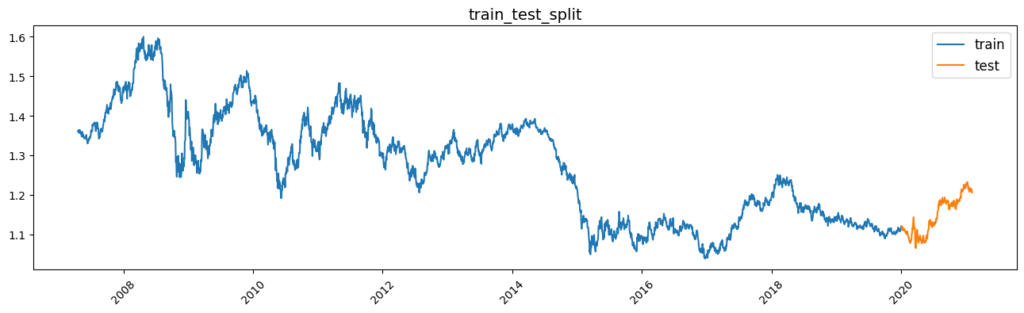

### Validation

# Validate while maintaining the sequence of time-series data, as next day's data may be mixed in the TRAIN and it is easy to over-learn when randomly partitioning with time-series data.

split_day = dt.datetime(2020,1,1)

df_tr = df_drop_add[df_drop_add['Date'] < split_day]

df_te = df_drop_add[df_drop_add['Date'] >= split_day]

X_train = df_tr.drop('Maguro', axis=1)

Y_train = df_tr['Maguro']

X_test = df_te.drop('Maguro', axis=1)

Y_test = df_te['Maguro']

### Range visualisation for train and test

fig, ax = plt.subplots(figsize=(16, 4))

ax.plot(X_train['Date'], X_train['eurusd_Open'], label='train')

ax.plot(X_test['Date'], X_test['eurusd_Open'], label='test')

ax.legend(fontsize=12)

ax.set_title('train_test_split', fontsize=14)

# ax.xaxis.set_major_locator(mdates.MonthLocator(interval=12))

# ax.xaxis.set_major_formatter(mdates.DateFormatter('%y/%m'))

ax.xaxis.set_tick_params(rotation=45)