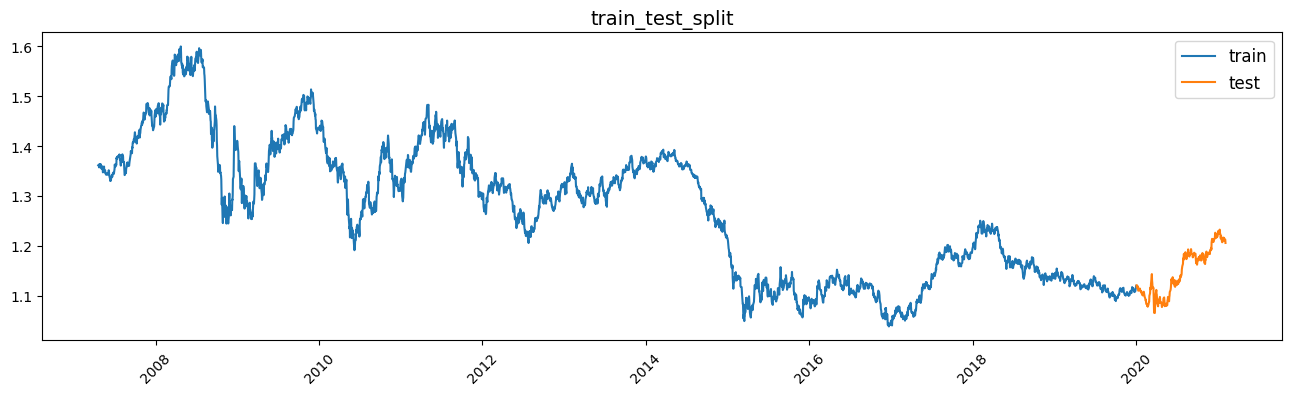

Forex Forecasting with Random Forests 4/N – Precision Rating

Economy

### Trade Simulation

def trade_simulation(dfx,leverage,start_balance):

i = 0

for index,item in dfx.iterrows():

# Margin required for 10,000 EUR (1 ticket) trade

dfx.loc[index,'margin_per_eur'] = item['eurusd_Close']*item['usdjpy_Close']*10000/leverage

# Bank balance

if i <= 1:

dfx.loc[index,'balance'] = start_balance

else:

dfx.loc[index,'balance'] = dfx.loc[index-1,'balance'] + dfx.loc[index-1,'profit_loss']

# Num

num = dfx.loc[index,'balance']/2/dfx.loc[index,'margin_per_eur']

if num>100:

num = 100

dfx.loc[index,'num'] = num

# Required Margin

dfx.loc[index,'margin'] = dfx.loc[index,'margin_per_eur']*dfx.loc[index,'num']

# Investment Residuals after Position Making

dfx.loc[index,'capacity'] = dfx.loc[index,'balance']-dfx.loc[index,'margin']

# Rate fluctuation tolerance

dfx.loc[index,'rate_fluctuation_tolerance'] = dfx.loc[index,'capacity']/(dfx.loc[index,'num']*10000)

# Profit and loss

if i <= 1:

dfx.loc[index,'profit_loss'] = 0

else:

dfx.loc[index,'profit_loss'] = dfx.loc[index-2,'pred']*(dfx.loc[index,'eurusd_Close']-dfx.loc[index-2,'eurusd_Close'])*dfx.loc[index-2,'num']*10000*dfx.loc[index,'usdjpy_Close']

i = i+1

return dfx

### Trade Simulation

def trade_simulation(dfx,leverage,start_balance):

i = 0

for index,item in dfx.iterrows():

# Margin required for 10,000 EUR (1 ticket) trade

dfx.loc[index,'margin_per_eur'] = item['eurusd_Close']*item['usdjpy_Close']*10000/leverage

# Bank balance

if i <= 1:

dfx.loc[index,'balance'] = start_balance

else:

dfx.loc[index,'balance'] = dfx.loc[index-1,'balance'] + dfx.loc[index-1,'profit_loss']

# Num

num = dfx.loc[index,'balance']/2/dfx.loc[index,'margin_per_eur']

if num>100:

num = 100

dfx.loc[index,'num'] = num

# Required Margin

dfx.loc[index,'margin'] = dfx.loc[index,'margin_per_eur']*dfx.loc[index,'num']

# Investment Residuals after Position Making

dfx.loc[index,'capacity'] = dfx.loc[index,'balance']-dfx.loc[index,'margin']

# Rate fluctuation tolerance

dfx.loc[index,'rate_fluctuation_tolerance'] = dfx.loc[index,'capacity']/(dfx.loc[index,'num']*10000)

# Profit and loss

if i <= 1:

dfx.loc[index,'profit_loss'] = 0

else:

dfx.loc[index,'profit_loss'] = dfx.loc[index-2,'pred']*(dfx.loc[index,'eurusd_Close']-dfx.loc[index-2,'eurusd_Close'])*dfx.loc[index-2,'num']*10000*dfx.loc[index,'usdjpy_Close']

i = i+1

return dfx

### Trade Simulation

def trade_simulation(dfx,leverage,start_balance):

i = 0

for index,item in dfx.iterrows():

# Margin required for 10,000 EUR (1 ticket) trade

dfx.loc[index,'margin_per_eur'] = item['eurusd_Close']*item['usdjpy_Close']*10000/leverage

# Bank balance

if i <= 1:

dfx.loc[index,'balance'] = start_balance

else:

dfx.loc[index,'balance'] = dfx.loc[index-1,'balance'] + dfx.loc[index-1,'profit_loss']

# Num

num = dfx.loc[index,'balance']/2/dfx.loc[index,'margin_per_eur']

if num>100:

num = 100

dfx.loc[index,'num'] = num

# Required Margin

dfx.loc[index,'margin'] = dfx.loc[index,'margin_per_eur']*dfx.loc[index,'num']

# Investment Residuals after Position Making

dfx.loc[index,'capacity'] = dfx.loc[index,'balance']-dfx.loc[index,'margin']

# Rate fluctuation tolerance

dfx.loc[index,'rate_fluctuation_tolerance'] = dfx.loc[index,'capacity']/(dfx.loc[index,'num']*10000)

# Profit and loss

if i <= 1:

dfx.loc[index,'profit_loss'] = 0

else:

dfx.loc[index,'profit_loss'] = dfx.loc[index-2,'pred']*(dfx.loc[index,'eurusd_Close']-dfx.loc[index-2,'eurusd_Close'])*dfx.loc[index-2,'num']*10000*dfx.loc[index,'usdjpy_Close']

i = i+1

return dfx

## Combine explanatory variables with predicted results of test data

# Data framing of eries type data

test_y2 = pd.DataFrame(Y_test)

test_y2['pred'] = model.predict(X_test)

# Prediction Result Storage

col = ['Date','eurusd_Open', 'eurusd_High', 'eurusd_Low', 'eurusd_Close', 'usdjpy_Close', 'Maguro', 'pred']

df_test_result = pd.merge(df_drop_add, test_y2['pred'], left_index=True, right_index=True)[col]

## Combining explanatory variables with the predicted results of train data

# Data framing of Series type data

train_y2 = pd.DataFrame(Y_train)

train_y2['pred'] = model.predict(X_train)

# Prediction Result Saving

col = ['Date','eurusd_Open', 'eurusd_High', 'eurusd_Low', 'eurusd_Close', 'usdjpy_Close', 'Maguro', 'pred']

df_train_result = pd.merge(df_drop_add, train_y2['pred'], left_index=True, right_index=True)[col]